TLDR

If you’re familiar with freight markets this will be very easy to understand. The thesis can be summarized this way:

Yellow LTL story + Truckload supply story = PAL story

For those who are not freight aficionados, PAL transports cars, it’s a weird area of freight with no other comps, it’s been massively under-earning.

In March 2025, the #2 player, union carrier Jack Cooper, went bankrupt. They were roughly 10% of US supply. This could have driven an epic cycle but auto demand softened and became more unpredictable (post liberation day), this lower demand offset the supply cut.

I believe we’re just at an inflection, I believe an incremental 10% of supply (20% total) is in the process of being removed for a variety of reasons: non-domiciled CDL ban, English language proficiency test, exits into truckload…

Management a couple of days ago has acknowledged that around 20% of supply is gone, and that demand now outstrips supply leading to higher pricing, that’s the holy grail of freight investing.

I believe at half the P/E multiple of peers, on mid-cycle numbers, the stock has 120-300% return potential.

Company overview

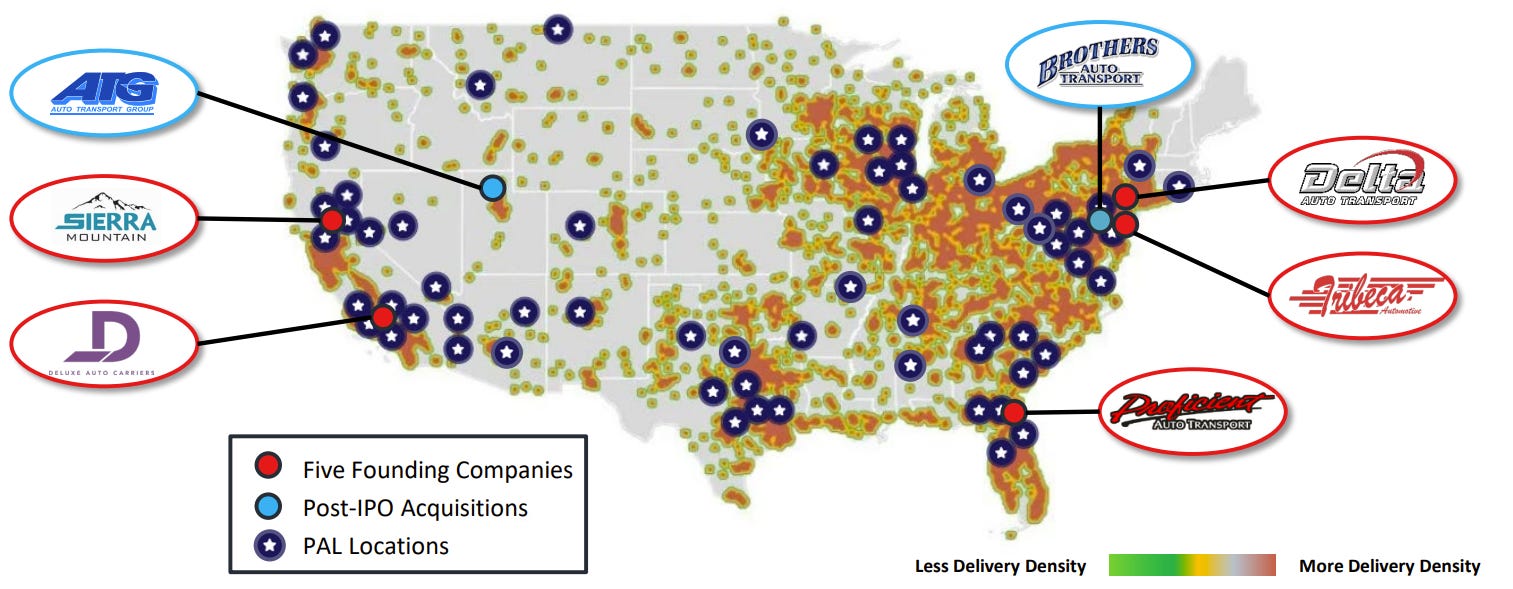

Proficient Auto Logistics is a transportation and logistics company focused on “auto-hauling”. What it means is they transport new cars to dealerships from factories, ports and rail yards. Their customers are the auto OEMs.

PAL was created as the merger of 5 regional carriers, which came public in May 2024.

The premise was, this is a niche unsophisticated area of freight, let’s build the pre-eminent roll-up in the space, become one of the few true national carriers, integrate best in class systems, and well… make money.

The management team is actually way too good for the size of this company. The CEO and architect behind the idea is Rick O’Dell. He was President & CEO of SAIA since 1999, during his tenure the stock 60x. Yes, that good. He’s actually still the Chairman of SAIA. For context, SAIA is a $12bn Less than Truckload carrier.

I won’t elaborate too much on the business, if you want more details read the investor presentation and the 10K for the nuances like what is company owned hauls vs sub-hauling, contract dynamics etc. I am going to focus on the value-added part.

It’s like any freight business, it’s volume x price, if supply > demand → price down and if supply < demand → price up.

Investment thesis

The idea is that we have seen a major supply cut (bankruptcy of Jack Cooper) which went un-noticed due to degradation in demand, and are now seeing a second major supply cut event in real time (like we’ve seen in truckload).

As demand is returning to normal, these supply cuts are becoming apparent, which will lead to higher pricing and volume for PAL, and much higher earnings.

I am going to compare both of these supply events to events that have recently transpired in the freight market, which both led to monster stock returns for their respective group. I believe PAL has both of these stories going on at the same time.

1 - Jack Cooper is the Yellow LTL story

I am going to make a parallel with a well known story that happened in freight, the impact of the Yellow bankruptcy on the Less Than Truckload “LTL” market.

The Yellow story

Yellow was a union LTL carrier, they were the #3 player in the US with 7% of the market. The company had been troubled for decades, accepting low priced freight and being the “irrational” player in the market.

In the summer of 2023, Yellow finally collapsed, it stopped operations and eventually declared bankruptcy. All the former Yellow customers had to find a new home for their freight which led to a massive rise in volumes and pricing power for the remaining carriers.

It was both a great short-term and long-term set up, 7% of the market went away, demand then outstripped supply which led to higher pricing in a fairly consolidated industry.

The stocks took off, it was an amazing trade:

The stocks peaked mid 2024 as that Yellow capacity ended up mostly coming back to the market after 90%+ of their terminals got sold back in auction to other LTL carriers, and lots of carriers also made large organic investments in supply.

So when Yellow went bankrupt, going long LTL was an amazing trade. Why do I talk about this? Because PAL has a very similar set-up that’s happened, but has gone un-noticed.

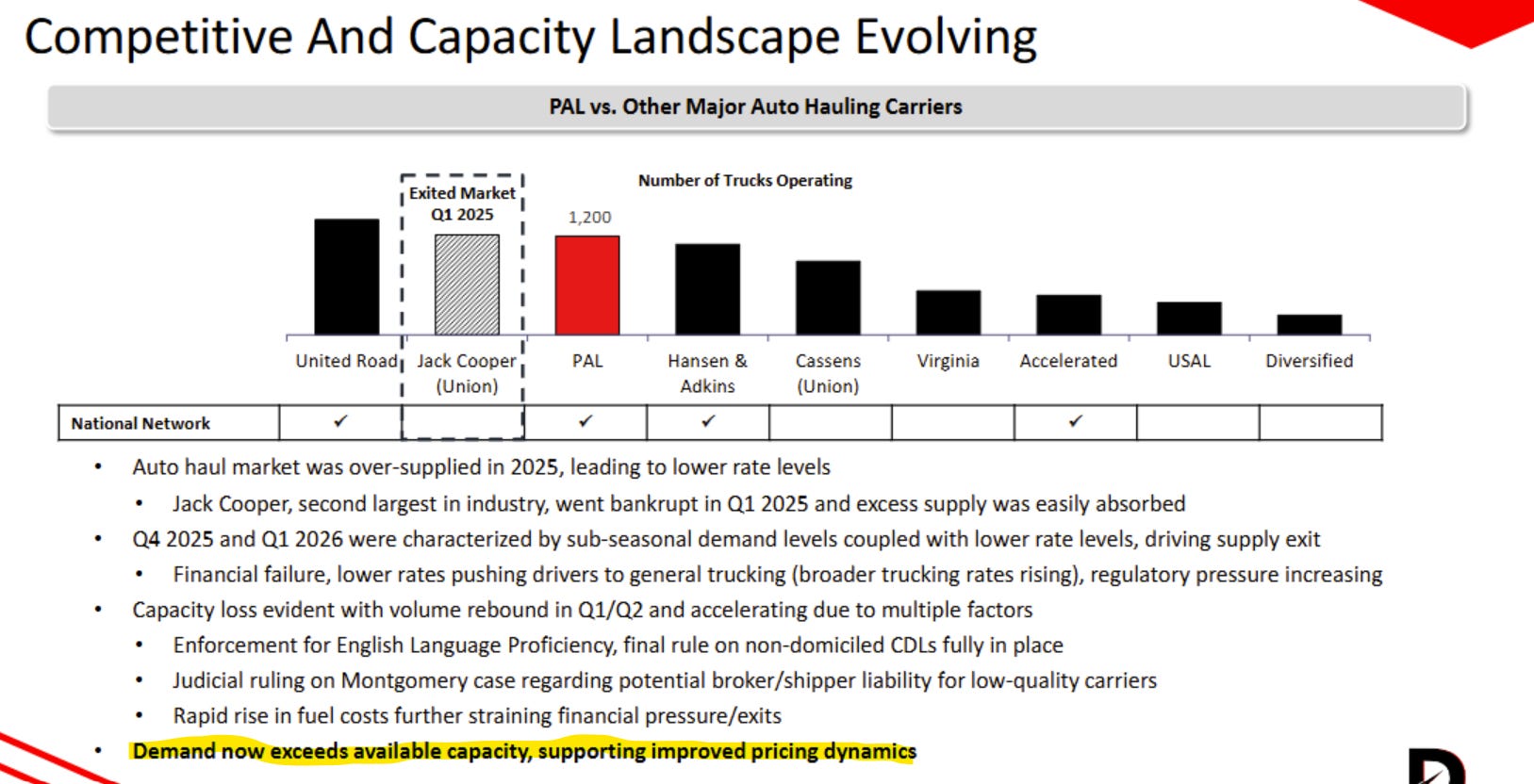

Jack Cooper is the Yellow of auto-hauling

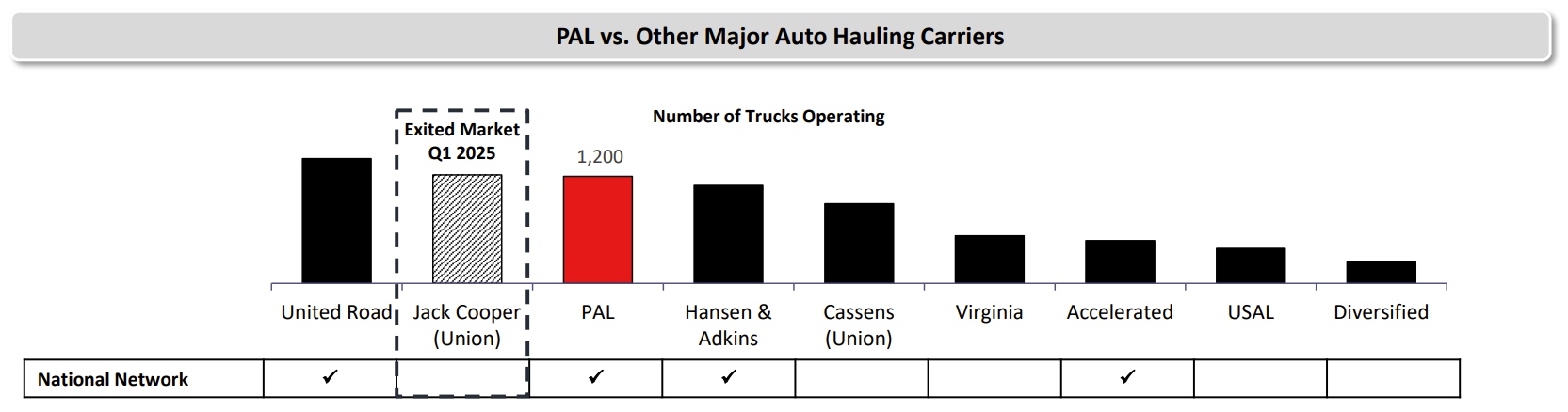

Jack Cooper was the #2 player in auto-hauling, an industry as consolidated as LTL, it was also a union carrier that had been under pressure for some time.

They represented roughly 10% of the market and ended up going bankrupt in March 2025. Their largest customers (Ford & GM) had to put a bunch of their business elsewhere, PAL won a good chunk of that.

Does this sound similar? Sounds like the exact same story as LTL.

I actually think it’s better, first Jack Cooper was bigger than Yellow in terms of supply, 10% vs 7%. But the big one is that the Yellow capacity ended up coming back to the market because demand for LTL services was healthy. Jack Cooper on the other hand, there was no demand for these assets, it’s just trucks not terminals, they were old, and most got either scrapped or sent to Mexico and are not coming back.

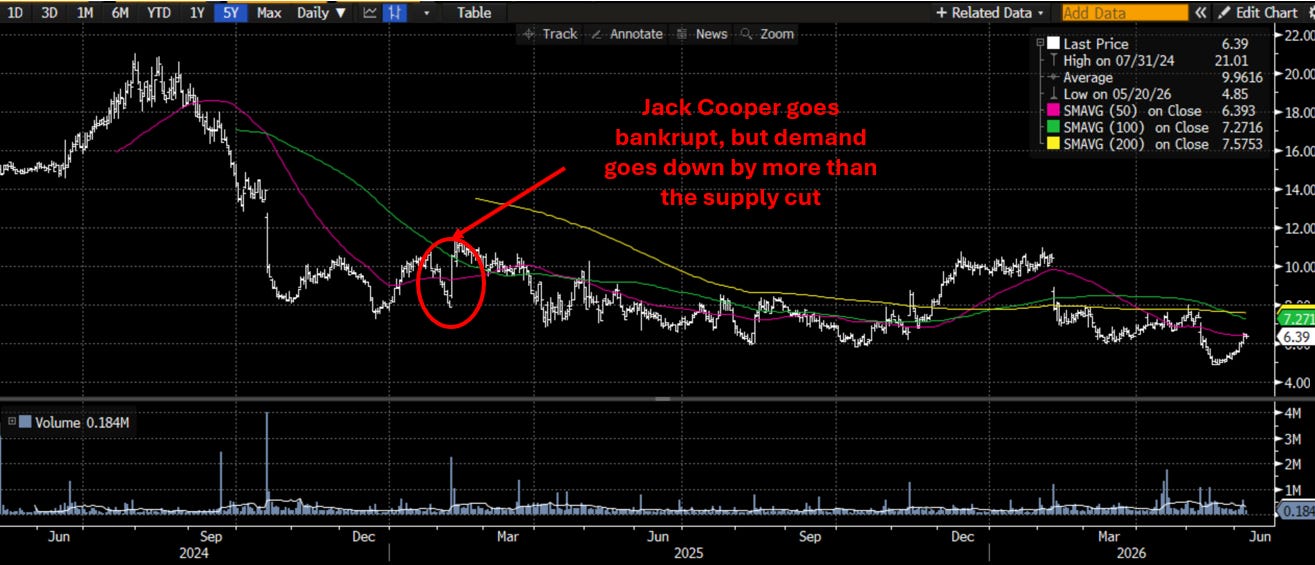

But this happened in early 2025, why didn’t PAL work by now then?

That’s because a month later Trump’s liberation day happened, demand for auto-hauling slowed down significantly, and while the 10% supply cut softened the blow, demand went down enough that supply/demand remained imbalanced. So when you’d have expected a big inflection in PAL’s numbers, they actually remained pretty shitty.

The thesis then became “when demand comes back this will be epic, but who knows when that is”. Unless… we saw more supply cuts.

2 - The truckload story is playing out in auto-hauling

Here comes the new piece of the story, what I think will drive the inflection, and which is just starting to emerge.

The truckload story

If you don’t follow freight, after a very difficult downturn, truckload stocks have roared back:

And this is driven by a real fundamental inflection:

What’s been driving this? Well while demand is getting a bit better, supply cuts are driving a large part of this move.

The primary underlying driver behind this is the Trump administration’s enforcement of various rules against foreign truck drivers which started in summer of 2025:

1 - Non-domiciled CDL crackdown. Non-domiciled CDLs were introduced in 2017 to provide flexibility for drivers who reside in a State but needed a license in another. The problem is that over time, non-US residents found this loophole, and used it to get CDLs. You then had foreigners, or even illegal immigrants, driving trucks. By cracking down on this, the Trump admin removed a lot of supply from the TL market. This has already removed around 3-4% of supply today but expected to be 10%+ in the coming years.

2 - English Language Proficiency enforcement. This rule has been around forever and is common sense but it has not been enforced under the Biden admin. This is removing even more capacity.

3 - Montgomery case. Freight brokers used to be shielded from liability, after a Supreme Court decision on the case in May 2026, a broker can be sued for having hired a negligent trucking company. This adds even more pressure on supply as brokers will be scared to work with dodgy operations.

Ok so this is great for truckload, but why does this matter for PAL? The truckload stocks started ripping in mid 2025 and PAL has been awful in that time frame, clearly PAL doesn’t stand to benefit from this right?

Why PAL will benefit from the same tailwinds as truckload

I believe PAL will benefit from the non-domiciled CDL, English Language Proficiency and to a lesser extent the Montgomery case.

On top of that, I think there is now a lot of drivers leaving to go work in the truckload market because rates are so much better, further tightening supply.

And business has been so tough in auto-hauling that I think some carriers have lost too much money and are exiting.

Ok so why hasn’t PAL gone up like the other truckload guys yet?

The reason why PAL hasn’t benefited yet is simple.

The same supply dynamics that happened to truckload are happening in auto-hauling, but we didn’t see it in the market because demand was particularly weak in late 2025 and early 2026. OEMs took down auto inventory levels late 2025, and weather sucked in January and February of 2026, so with demand down, you didn’t notice the supply cuts.

The market took this as “auto-hauling doesn’t have the same tailwinds”, and the market has no real live pricing data like in truckload to disprove it.

But then the Q1 26 call had the first signs of an inflection:

CEO: “The rebound in volumes in March and April made capacity tightening more evident, exposing underlying supply loss that had previously been less visible. Supply losses appear to be driven by a combination of factors including financial pressure from low volume, compounded by relatively weaker rates, increased relative scrutiny or regulatory scrutiny and driver migration towards other forms of trucking as the broader trucking rates have improved. At the same time, supply conditions have increased spot market opportunities.

[…] So this is clearly a turning point in the auto haul market.”

And this exchange:

Analyst: "I want to focus in first on some of what you mentioned in the opening remarks around the supply pressure. Certainly welcome news. But wanted to see how you’re thinking about that in terms of spot, what you’re seeing in terms of spot pricing pressure in the market right now?”

CEO: “In terms of the spot environment in Q1, it was an absolute flat line during the month of January and February, as you would expect. In March, when volume levels returned and the supply exit became more visible, there was a market increase in spot opportunity, but there was lack of availability to participate in those spot opportunities on a widespread basis. So what we experienced was a couple of percentage point increase in our participation in the spot market at rate levels of premiums that were frankly better than what we’ve seen in the last couple of quarters, but still immaterial on an overall revenue basis compared to the overall portfolio.”

What does this mean? To me it means “we didn’t know it was happening cause volumes sucked, when they became more normal in March/April, it became apparent that a lot of supply went away, but for now we’re not too sure.”

Ok so this is pretty good and interesting, the same tailwinds as the ones in truckload seem to be starting to remove supply in auto-hauling too. But who knows how meaningful it’ll be and where we stand on supply/demand?

3 - Signs that the inflection is now

So Jack Cooper cut 10% of supply, but demand went down more. And now we have more capacity exits as a potential tailwind, similar to what happened in truckload, but we’re not sure how meaningful it is.

That’s what the status quo was in early May when PAL had their Q1 26 call.

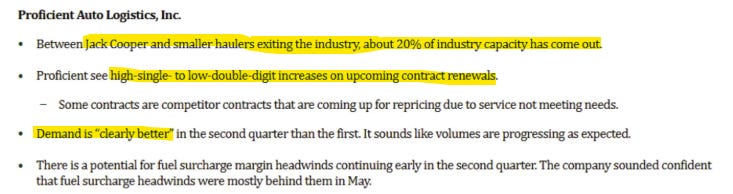

Then something fascinating happened, 3 weeks later, PAL gets on the road and seems to have a much clearer picture of how “real” the supply exits have become in recent weeks. This is buried in a conference recap from the William Blair Growth stock conference that happened 4 days ago:

“20% of industry capacity has come out”, this means it’s no longer the 10% supply cut of Jack Cooper, there’s an incremental 10% that’s come out in the last couple of months driven by the various tailwinds I talked about earlier (non-domiciled CDL, English proficiency, unprofitable players exiting).

This is a giant capacity shift, 20% of supply came off in a year. At the same time demand has inflected back to normal. So what does this mean?

Demand > supply for the first time in multiple years, that means pricing power:

“Proficient sees high-single to low-double-digit increases on upcoming contract renewals”

This is a massive shift that has just happened in recent weeks. The investor deck they published confirms this, this is completely new to the deck:

They also show the steep improvement in demand:

Why am I so excited?

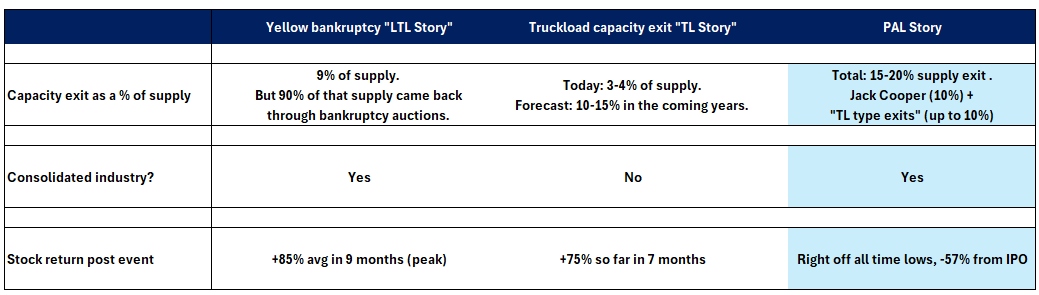

Let me put it in context, LTL saw 7% of capacity exit temporarily, most of it came back, and stocks returned 100% in less than a year at their peak. Jack Cooper is a bigger deal than this.

Truckload stocks are up 50-100% on roughly 4% capacity cuts (with expectation of more) in the past 7 months driven by non-domiciled CDL rule change and English proficiency test enforcement.

Proficient is benefiting from BOTH of these similar tailwinds, 20% of supply is coming out and demand is re-inflecting back to normal. Management just had a massive tone shift and no one has noticed with a stock near all time lows since this tone shift happened at a non-webcasted conference 4 days ago.

Here’s an illustration of the comparison between PAL and the other two successful freight stories:

I am being conservative with my 15-20%, management outright says 20% of supply is gone.

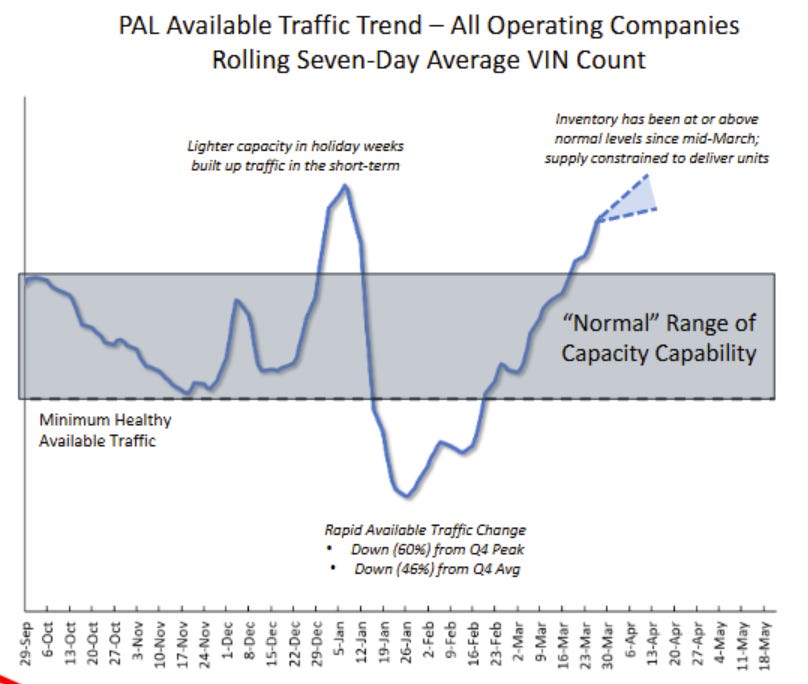

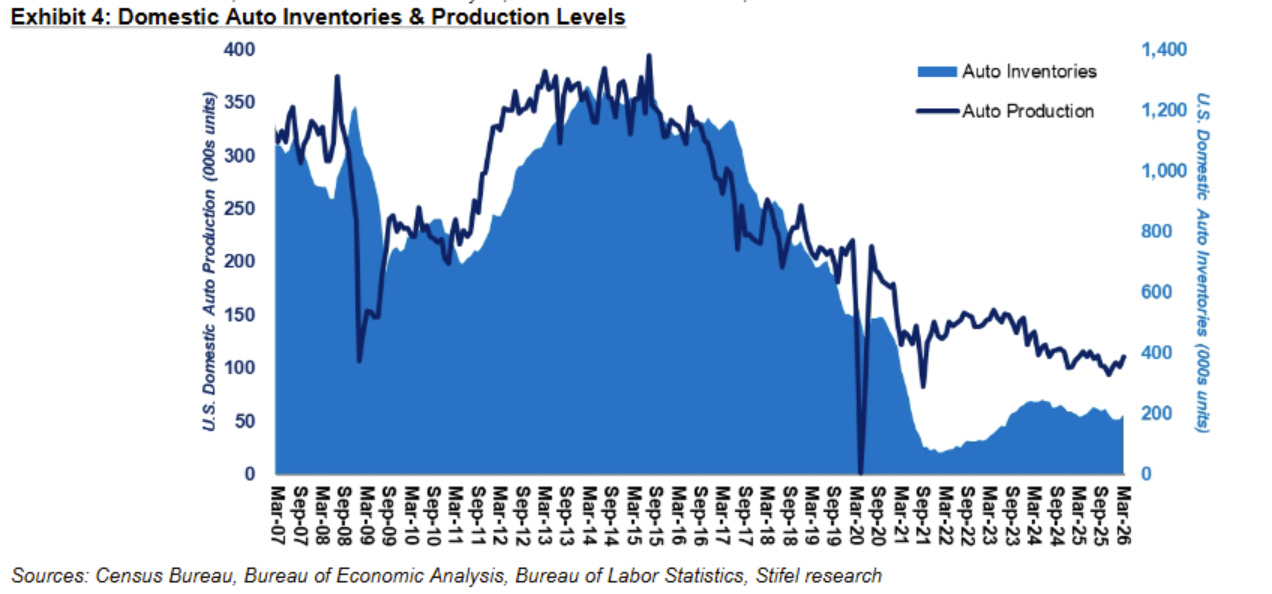

On top of that demand is actually getting good again, as management said “demand is clearly better” after a tough January and February. I am assuming it remains sort of flat from here. And then there’s always the optionality of demand getting better which no one is pricing in. Take a look at this chart and make up your own mind:

So anyway, that’s the story, 20% of supply has come out, demand is normalizing, and management has acknowledged that demand > supply = higher prices, and it’s just starting to happen.

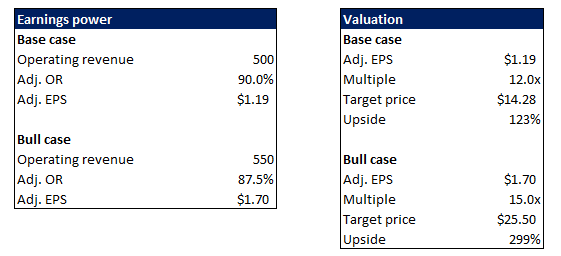

Valuation & numbers

PAL today is 1.5x levered, trading sub 6x EBITDA on what I believe are trough numbers.

As we established earlier, things are just inflecting. I am not expecting a particularly good Q2, I am expecting better revenue, but some cost pressure due to diesel prices, these will be a non-event soon because of pass-throughs but sometimes there’s a lag between when you pay and when you recover.

Pricing is apparently now up around 10%, but this will only flow through on renewals. I expect them to talk about how fast the environment is improving, and expect at some point in H2 that results will start to inflect.

They’ve often floated an achievable Adj. Operating Ratio (1 - EBIT margin) of mid to high 80s, that slowly drifted to high 80s to low 90s as demand turned and they wanted to be a bit more conservative, but I think the mid to high 80s is likely still feasible.

I think I am being fairly reasonable here, embedding mid-cycle not up-cycle numbers.

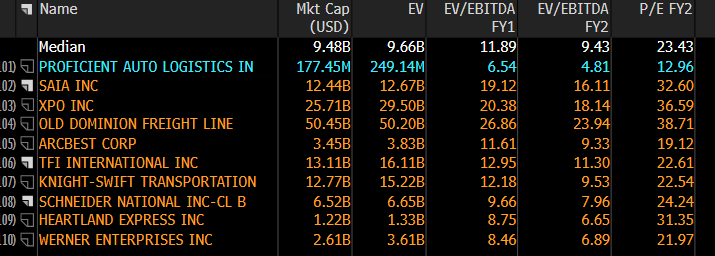

Multiple wise too, there’s two peer sets that are relevant here, Truckload “TL” and Less Than Truckload “LTL”.

The LTL guys (SAIA, XPO, ODFL, ARCB, TFII) trade on next 24 months earnings at 30x EPS and TL guys trade at 25x EPS. I would argue the TL group typically trades at lower multiples than that on mid cycle.

I think clearly I am being very conservative with my 12x and 15x EPS given Truckload is a worst business than auto-hauling by a wide margin. One could think $1.5 x 20x = $30 is reasonable, but we don’t need to get this bold.

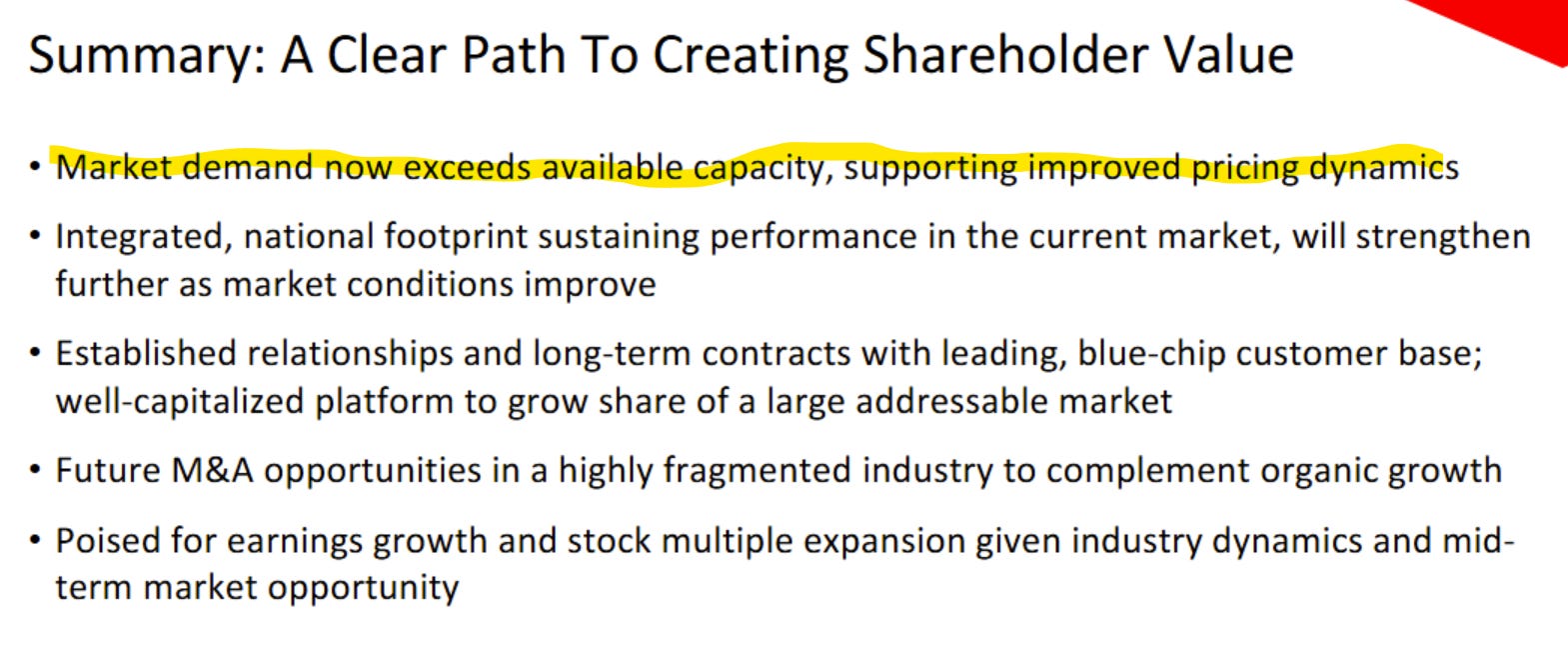

Conclusion & risks

So PAL is right off the lows, trading cheap on trough numbers, and is inflecting in real time. In the past few days management confirmed that nearly 20% of supply has/is coming out, and that now demand > supply driving higher pricing. There’s two prior set-ups similar to this and both led to explosive stock returns.

What could go wrong? Well there’s auto in the name, I am not assuming particularly good demand but if auto sales collapse it’ll be bad. The supply cuts might take a bit longer than expected to kick in given the multi-year contract nature of the business. And in the very near-term there could be a bit of margin pressure due to diesel pass-through lags.

Disclaimer: I own shares in Proficient Auto Logistics. I may buy or sell at any moment without disclosing it. This is not financial advice this is for entertainment purposes only. Please consult with a financial advisor.

This I like. Excellent close reading on the management tone flip. Their confidence from the second wave of supply tightening looks very recent like you say: CFO said in February “we never rule out share repurchases, but that’s probably at the lower end of the priority list at this point” then the 10-Q shows they quickly slurped up $500K worth at ~$6.25 in March. It’s a fraction of the authorization but tracks with ‘they know’.

Interesting. My big question is why the industry doesn't have more competition. LTL is very complex and capital intensive. This seems closer to plain TL, with a bit of specialized equipment that is still relatively cheap in the scheme of things.