TLDR

Assertio is a pharmaceutical company with a drug IP protected through 2039 growing 30%+ with nearly 30% EBITDA margins

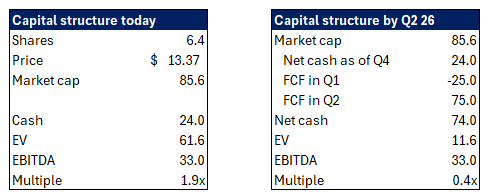

Over the next 2 quarters ASRT will collect $50M of FCF on an $85M market cap

The company trades at 0.3x 2026 EBITDA

Company overview

Assertio is a commercial pharmaceutical company, they aren’t drug R&D guys, they’ve acquired the right to many drugs over the years and focus on commercialization. These drugs usually start out as patent protected and eventually go generic.

Assertio today is mainly one drug, Rolvedon (70%+ of revenue). Here’s a bit of an overview of what it does:

When cancer patients receive chemotherapy, the drugs don't just kill cancer cells, they also wipe out the bone marrow's ability to produce white blood cells. The specific white blood cells that get depleted are called neutrophils, which are your body's front-line infection fighters. When neutrophil counts crash (a condition called neutropenia), patients become dangerously vulnerable to infections. A fever in a neutropenic patient is a medical emergency called febrile neutropenia, it can be life-threatening and often requires hospitalization.

This is one of the most common side effects of chemotherapy, and it frequently forces doctors to delay or reduce chemo doses, which undermines the cancer treatment itself.

Now what does Rolvedon do? It’s from a class of drug called G-CSF stimulants, the original was Neupogen approved in 1991. Rolvedon is a newer improved version. It’s essentially a signal to your bone marrow telling it to rapidly produce more neutrophils. It mimics a natural protein your body already makes called G-CSF (granulocyte colony-stimulating factor), which is the hormone that normally triggers neutrophil production. By flooding the system with this signal after chemo, you can dramatically shorten the window where the patient is dangerously vulnerable to infection. Rolvedon was developed by Hanmi Pharmaceutical and licensed to Spectrum Pharmaceuticals which Assertio acquired.

They have 2 other drugs that are a lot less important, Indocin and Sympazan.

Indocin has gone generic and has been declining fairly fast, it used to be $100M of revenue in 2022 and is now down to $19M.

Sympazan is stable to growing. It’s a neurological drug but I won’t focus on it too much because it’s only $11M of revenue and it’s being managed for cash not for growth.

The opportunity

Assertio today is in the final process of lapping two weird quarters before collecting a bundle of money in Q2 2026 (I explain why later in the pitch).

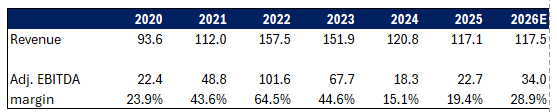

At the same time EBITDA is meaningfully inflecting and still understates the earnings power of the company.

You’re paying sub 1x EBITDA by Q2 26 for a drug asset that’s IP protected through 2039 that just grew at the point of sale 32% in 2025:

EBITDA is inflecting and revenue is stabilizing as old drugs roll-off and Rolvedon grows:

Why the opportunity exists

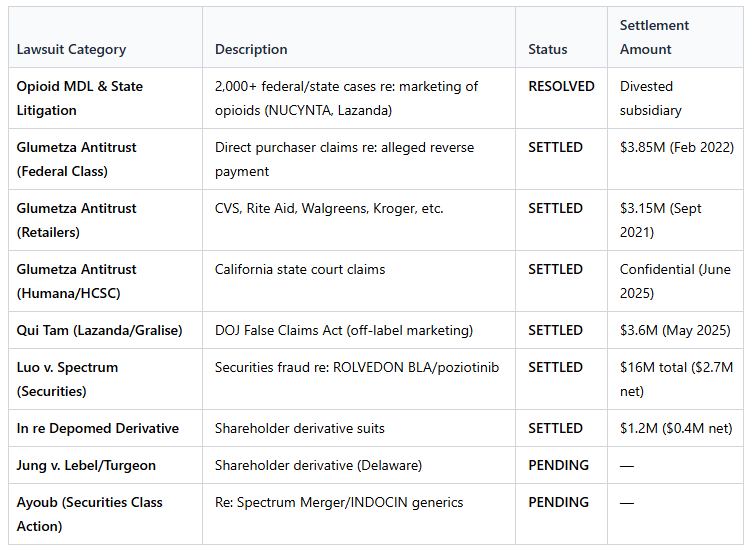

Seems too good to be true? I agree, so let me explain to you the shitshow of old Assertio and why no one is looking at the company. The main issues are as follows:

Opioid lawsuits

Investor lawsuits on the back of a deal with Spectrum Pharmaceuticals

Holding company structure and strategy

Q3 2025 to Q2 2026 are very confusing

Opioid lawsuits

Assertio started out as a company called Depomed in 1995, an opioid pain drug company, they ended up acquiring for $1bn a drug called Nucynta from Johnson & Johnson in 2015, another blockbuster opioid painkiller. That turned out to be an awful idea since the timing aligned with the opioid epidemic and subsequent lawsuits. This wound up being a shit deal, they sold it in 2020 for $375M, but it ended up costing them money years later.

Between 2013-2017 the government alleged that Depomed (now Assertio) were too aggressive on the marketing to doctors when it came to pushing their fentanyl products, similar to a lot of the high profile opioid cases.

Then came an avalanche of lawsuits, a securities class action, shareholder lawsuits, State and Government investigations and multi-district litigations.

What did it cost them? Tens of millions in legal fees every year for years, a $3.6M settlement and damage to drug sales.

This is now fully behind them as of early 2025, to close this whole chapter, Assertio transferred all of its remaining legal liabilities by paying someone to take it over for $8.2M. So the cash drag from the settlements is over, and the ongoing legal fees are over as well.

Spectrum Pharma deal and subsequent lawsuits

In 2018 they rebranded to Assertio Therapeutics, and in 2020 became a holding company, the idea was they’d become a big roll-up of a bunch of different drugs. Their first big move was merging with Zyla Life Sciences which brought them a couple of drugs including Indocin and Otrexuo. They then kept acquiring and licensing drugs like Sympazan and some others.

And then in April 2023 they did an all stock deal for $250M to acquire Spectrum Pharmaceuticals. This was a clusterfuck that led to a bunch of lawsuits that spiked the legal costs at Assertio and led to a bunch of settlements (a large chunk insured). The lawsuits are centered on poor disclosures both at Spectrum and Assertio on the deal disclosure.

Spectrum was what got them Rolvedon.

Spectrum itself had been sued in 2022 in Christansen v Spectrum, alleging that they mislead investors with their phase 3 trial drug.

Then the Spectrum merger created a couple of investor lawsuits, you know the bullshit PR you see on every stock that’s down more than 20% like “XYZ lawsuit encourages investors in ABC stock to reach out”? They’re fishing for class actions looking for a settlement of a couple million bucks.

In this case, Assertio paid Spectrum shareholders in shares, but those shares turned out to be way overvalued because their main drug, Indocin, was starting to face steep competition from generics so sales imploded and so the $250M deal price soon became not much.

What this meant is uncertainty on how much true net cash is once the lawsuits are over, and also a bunch of legal costs.

For all intents and purposes today, these are essentially all gone:

The most dangerous one was the opioid one because of its implication. A couple of quarters ago management had guided to minimal settlements and dismissals and that’s essentially what happened. Also they hold significant D&O insurance so the net amounts are fairly negligible.

There’s only two left:

Ayoub: same point as the others, old management didn’t warn that Indocin sales would get hurt by a generic. This used to be called Shapiro v. Assertio, essentially the law firm had convinced a guy who owned shares, Mr Shapiro, to try and sue the company, and then that guy ended up dropping out, likely thinking it’s too superficial of a case, so the class action guys desperately tried to convince any former shareholder to join their suit (I know for a fact they aggressively reached out to a bunch of shareholders and it took them months to convince someone to join). The case is waiting on the result of a motion to dismiss. Even if it was real which I doubt, the settlement would be minimal, low single digit millions and likely covered by D&O insurance, we have a lot of precedent from prior cases and this was by far the weakest.

Jung v Lebel/Turgeon: this is a shareholder suing on behalf of the company against the old executives, the company is a nominal defendant. This is highly unlikely to be an issue because of that.

The best proof that we’re essentially at the end of the lawsuits is what management guided to for 2026:

“Turning to operating expenses. Reported SG&A expenses were $13.1 million, down from $21.4 million in the prior year, reflecting lower legal expenses following completion of litigation-related initiatives” - Q4 2025 earnings call

“However, we do generally see a step-down in the adjusted SG&A figures, when you look at it, excluding stock compensation, D&A, et cetera. We do see a step-down from '25 to '26, especially given the de-risking from a litigation expense perspective” - Q4 2025 earnings call

Prior management was awful

I feel like I don’t need to explain why.

Here’s where we stand today tho. Everyone from the old guard is gone, and deep in the organization too not just the C-suite. The new management team is looking very solid especially for a company that size:

The new CEO is Mark Reisenauer, he is very legit unlike the prior clowns. He was a GM at pharma giant Abott. He worked for a biotech company called Micromet as Chief Commercial Officer which ended up getting acquired for $1.2bn in 2012 and got FDA approval in 2014, a huge success.

Most recently he spent 13 years at Astellas Pharmaceuticals focused on the US oncology business as President of the division. Astellas is a publicly traded Japanese pharma company (4503 JT) worth $30bn with $3.7Bn of EBITDA.

He was in charge of the commercialization of Xtandi which got FDA approval in 2012, a prostate cancer drug. He took that business to 50%+ market share, reaching nearly $5bn of revenue in 2023 and $2.5bn of EBIT.

The guy is very legit, and a great fit as a commercial oncology specialist (Rolvedon is an oncology drug), having run much larger entities very successfully.

The CFO is also new and has your typical big 4 into corporate accounting background.

Q3 2025 to Q2 2026 are very confusing

The company came out with what I thought was incredibly strong EBITDA guidance for 2026 and the stock is only up 10% (in a rough tape). I believe a big reason why is that the results are quite confusing if you don’t have context.

Assertio was set up as a holding company which came with a bunch of extra costs and complicated supply chain. The new management team is right-sizing these to become more profitable. Rolvedon was still under the old Spectrum structure, they used different CMOs, used multiple logistics guys, and had independent wholesaler agreements and a different National Drug Code “NDC”.

In order to make that transition completely smooth for the customers and patients, they shipped 3 quarters worth of end demand in Q3, which led to a monster amount of revenue and EBITDA. In order to do that, they had to give favorable working capital terms to their customers: payment by Q2 2026 on their receivables, and ASRT has to pay for the inventory and the rebates upfront.

What it means is this:

Q3 25: huge sales of Rolvedon worth 3 quarters worth of demand, great for EBITDA, unchanged for cash

Q4 25: $30M FCF burn since you have 0 Rolvedon sales and you pay for the inventory and rebates upfront

Q1 26: $25M FCF burn, still 0 Rolvedon sales

Q2 26” full quarter of Rolvedon sales, and you collect around $75M of accounts receivable

I encourage everyone to double check for themselves on the calls and looking at the balance sheets, you can clearly see that ARs are abnormally high.

So you see an amazing guidance for 2026, and yet a horrible quarter on revenue and FCF. This will all resolve in Q2 26 when you’ll have a monster FCF quarter, and normal EBITDA.

What that means as well is that management’s guide of $30M+ of EBITDA at the midpoint, only includes 3 quarters worth of Rolvedon sales, their main drug. This means the real EBITDA run rate is $40M+.

Also worth highlighting that Rolvedon was $68M of revenue in 2025 and management is targeting $100M+ of Rolvedon sales medium term.

Risks

There’s two main risks to me, mitigated by the fact that you’re paying next to nothing for the company.

Rolvedon competition

Listen I am not a pharma expert, Rolvedon competes against multiple other drugs, it’s IP protected for over a decade but it doesn’t mean they’re the only game in town. So far sales have been really solid (30%+ end demand growth in 2025) but that could turn.

Management blows part of the cash on M&A

Ok so ASRT has a lot of cash, they’ll have a ton of cash by Q2 26, and they’re profitable so the company is dirt cheap. Cool. What are they going to do with the cash?

I wish the answer was “we’re putting everything into buybacks” but it isn’t.

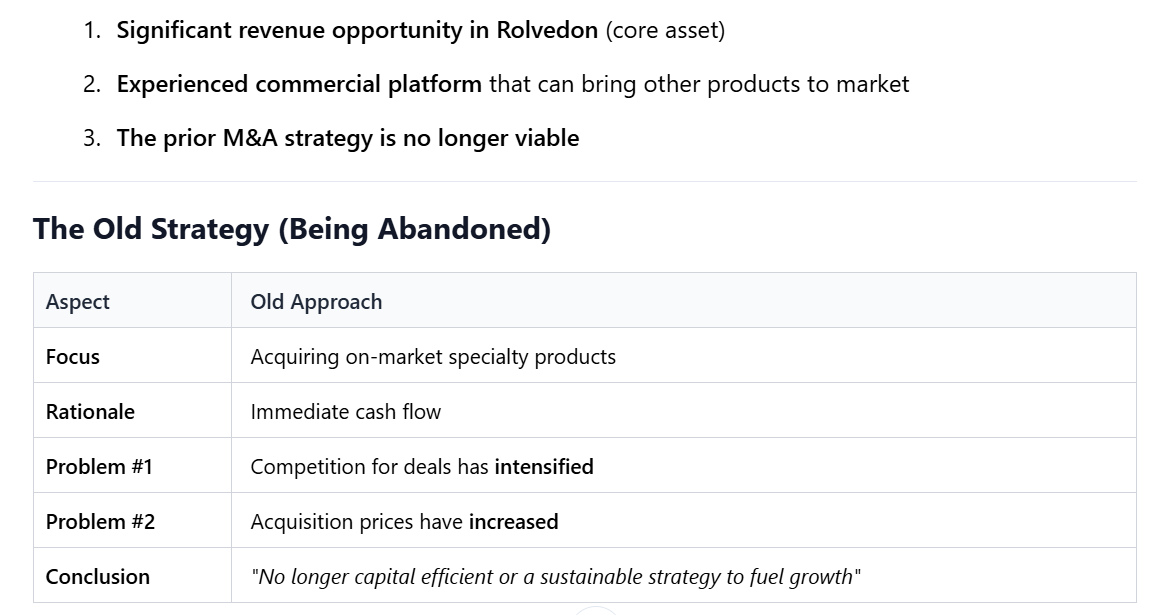

The new CEO’s strategy is this:

I totally agree with this, and I think everyone does, so why the risk? Well he’s ruling out the old stupid M&A playbook, but he’s not walking away entirely from investing in the business, which makes sense given he comes from much larger entities and came to run this little microcap.

His view is that they should pursue individual product acquisitions, commercialization agreements, licensing or technology agreements or potential M&A.

So hold up, he said the old M&A strategy is bad, and now he wants to do M&A? His underlying thought is this, they have the commercial infrastructure to market oncology drugs (aka Rolvedon), if they can add more oncology drug volumes through the same opex base they’d scale really nicely and it’d be very accretive to margins.

The idea is not to abandon entirely the idea of acquisition, but to consider them alongside licensing in a targeted way, in complementary products that use their existing infra, no longer a holdco strategy.

“On the BD side, we're going to be much more focused on finding opportunities that leverage our existing Rolvedon footprint and capabilities. Expanding our presence in oncology is a natural next step for us."

Here’s what bugs me tho, he said he was open to advanced “development stage assets”, read pre-phase 3 approval. This becomes a different kind of investment since capital allocation becomes high risk high reward.

Now listen, the guy is legit, he’s been through two very successful FDA approvals that turned into blockbuster drugs, but at the end of the day, it’s a bit of a gamble.

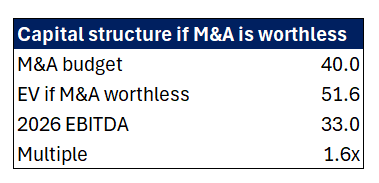

So how do I get comfortable with it? I have talked to a couple of people who have been in contact with management, they don’t plan to blow all the cash on deals, it’ll be measured, it might just be licensing, and if it is M&A, it’ll be a portion of the cash on the balance sheet, something like $30-50M would be the so called “budget”. Well, let’s just get overly punitive, say the deal is awful, it’s pre-commercial, it doesn’t get approved and it’s worthless (harsh given the guy running it), then how does our investment do?

Ok well I can pay 1.6x 2026 EBITDA instead of 0.3x for the growing Rolvedon business. Pretty assymetric.

And then what if it ends up being accretive? Well I’ll buy myself something nice.

Valuation

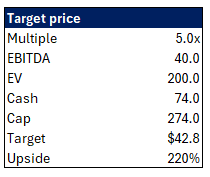

I keep it simple:

$40M of EBITDA is based on 2026 guidance but counting a full year of Rolvedon sales.

5x is out of my ass, likely should be more since Rolvedon is IP protected through 2039, but IP protected doesn’t mean Rolvedon doesn’t have competition, it definitely does, so you never know what could happen.

Today you’re paying nearly $0 of EV for this business generating $30M+ of EBITDA.

Disclaimer: I own shares in Assertio. I may buy or sell at any moment without disclosing it. This is not financial advice this is for entertainment purposes only.

How does one find these setups? Impressive ngl. Well played.

Do you have access to IQVIA or Symphony to track sell through data ?